Institute

louis

Bachelor

louis

Bachelor

“L’ILB aligne excellence scientifique et défis du réel”

Research programs

Investment for the future

The center of excellence in financial research, innovation and expertise.

Partners & Partnerships

+400 researchers

.

90 companies

.

60 research chairs

.

33 academic institutions

.

+400 researchers

.

90 companies

.

60 research chairs

.

33 academic institutions

.

Our events

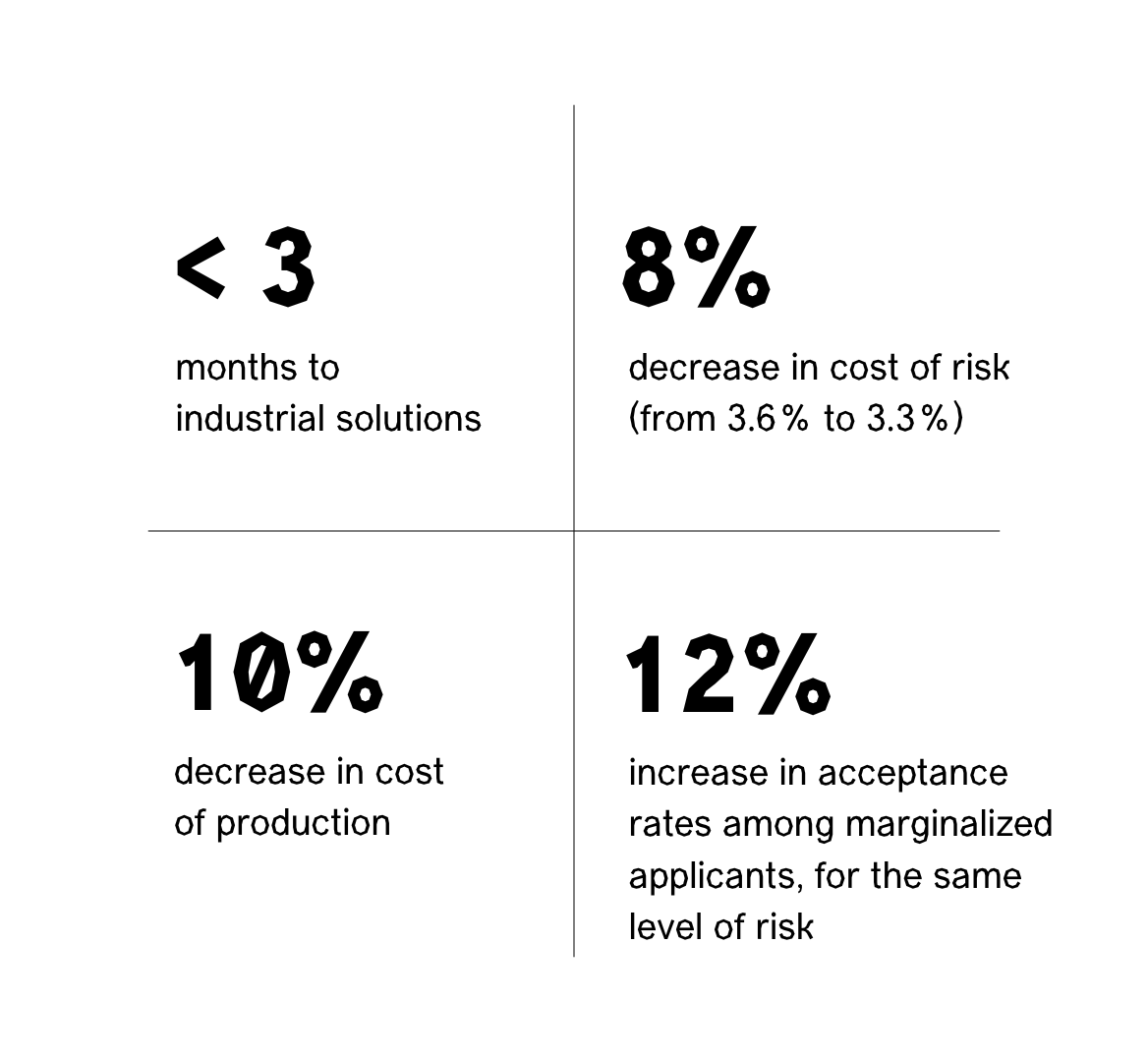

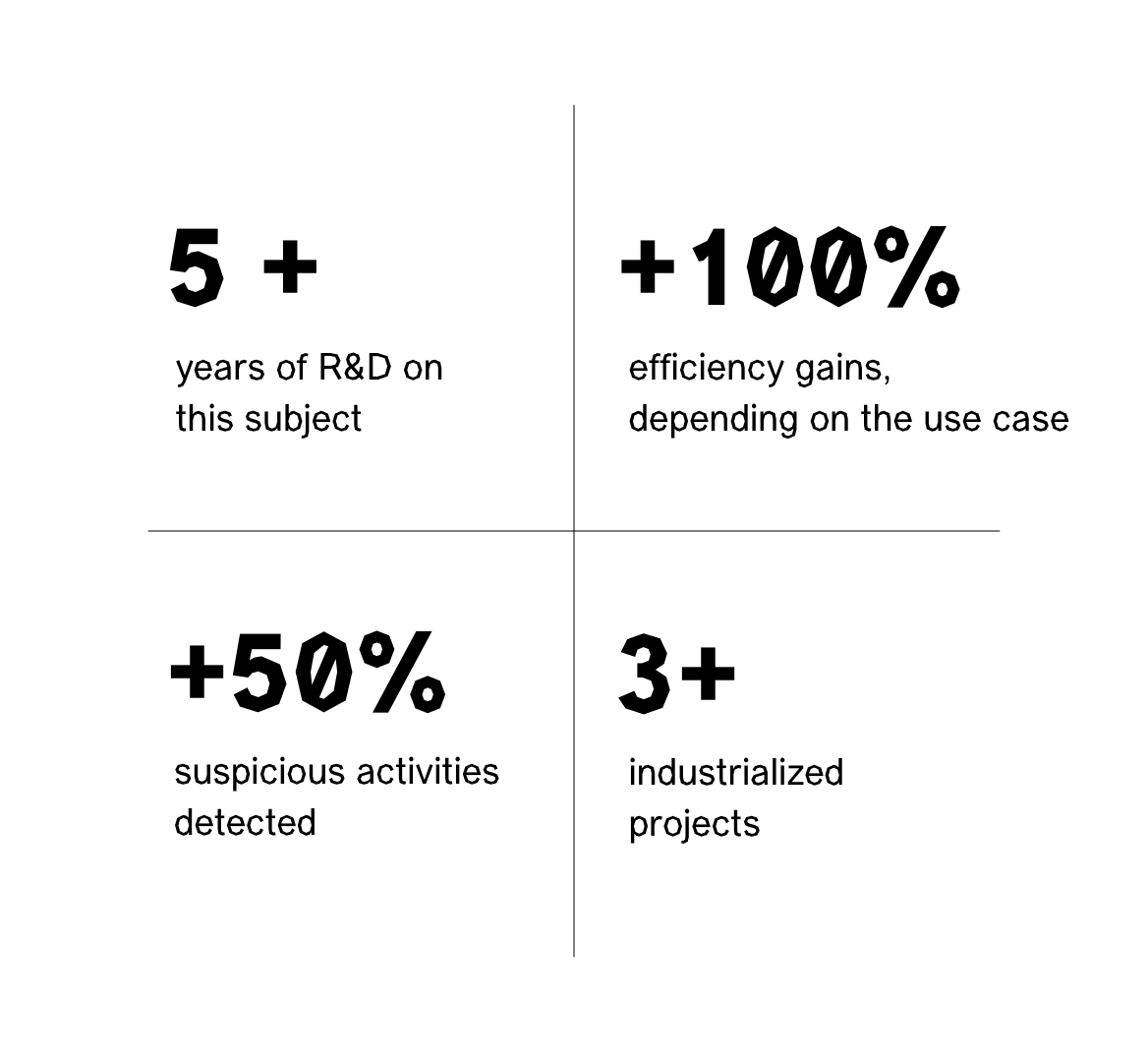

Supporting the digital transformation of the financial industry with R&D data science projects